Best for: Fintech companies that need secure, compliant, and reliable infrastructure without slowing down engineering teams.

Key verticals: Fintech, payments, lending, digital banking, wealth management, insurance technology, B2B financial platforms

Key platforms: AWS, Google Cloud, Microsoft Azure, Kubernetes, Docker, Terraform, GitHub Actions, GitLab CI, ArgoCD, Helm

Relevant strengths: Fintech DevOps, secure CI/CD, cloud infrastructure, Kubernetes, PCI DSS infrastructure, SOC 2 controls, observability, incident response

Best for: Banks, insurers, and financial services organizations modernizing legacy platforms and moving toward cloud-native delivery.

Key verticals: Banking, insurance, capital markets, financial services, manufacturing

Key platforms: AWS, Microsoft Azure, Google Cloud, Kubernetes, cloud-native platforms, CI/CD tooling

Relevant strengths: Banking expertise, DevOps transformation, cloud engineering, automation, cloud modernization, secure cloud foundations

Best for: Payments, banking, wealth management, and financial platforms that need large-scale engineering, cloud modernization, and operational support.

Key verticals: Payments, banking, finance, insurance, healthcare, technology, retail

Key platforms: AWS, Google Cloud, Microsoft Azure, cloud-native platforms, managed cloud environments

Relevant strengths: Cloud engineering, managed cloud, software modernization, financial services delivery, DevOps, application management

Best for: Financial services companies that need product engineering, cloud modernization, DevOps support, and long-term technical delivery teams.

Key verticals: Financial services, fintech, software, telecom, technology, regulated digital products

Key platforms: AWS, Google Cloud, Microsoft Azure, Kubernetes, Docker, Terraform, CI/CD tools

Relevant strengths: Financial software development, regulated delivery, cloud migration, DevOps, Kubernetes, managed services, modernization

Best for: Latin American banks, fintech companies, and financial institutions building or modernizing digital financial products.

Key verticals: Banking, financial services, fintech, insurance, enterprise IT, digital products

Key platforms: Cloud platforms, DevOps tools, automation, observability, digital banking infrastructure

Relevant strengths: DevOps, cloud platform services, IT operations, financial services, digital banking, nearshore delivery

Best for: Financial services companies that need managed cloud, DevOps, cloud security, and 24/7 infrastructure support.

Key verticals: Financial services, healthcare, public sector, enterprise IT, technology companies

Key platforms: AWS, Microsoft Azure, Google Cloud, private cloud, hybrid cloud, managed infrastructure

Relevant strengths: Managed cloud, cloud security, DevOps & CI/CD, monitoring, managed SOC, compliance support, cost optimization

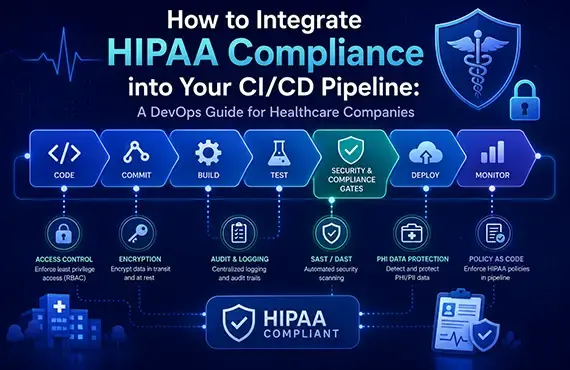

Do not accept a vague answer. Ask for examples involving payments, banking, lending, insurance, wealth management, financial data, or regulated financial software.

The goal is to understand whether the provider has worked in environments where auditability, access control, security, and reliability were central requirements.

A strong answer should include security scanning, approval workflows, environment promotion, change logs, role-based access, secrets management, artifact traceability, and automated evidence where possible.

If the provider treats compliance as a manual checklist after deployment, that is a warning sign.

Fintech companies need clear controls around who can access production, how access is approved, how long it lasts, how it is logged, and how it is reviewed.

Ask about least privilege, temporary access, break-glass procedures, identity providers, audit logs, and separation of duties.

A good partner should be able to describe incident detection, escalation, communication, rollback, root-cause analysis, post-incident review, and evidence collection.

In fintech, incident response is not only an engineering process. It can also become a compliance and customer trust issue.

The best fintech DevOps systems produce useful evidence automatically through normal engineering workflows. This includes deployment history, infrastructure changes, access logs, security scan results, approval records, and monitoring data.

If evidence has to be reconstructed manually before every audit, the DevOps process is not mature enough.

back to top